For value investors to understand the strength of a company in terms of assets and liabilities, they must first learn how to read and understand a company’s balance sheet.

What is the balance sheet?

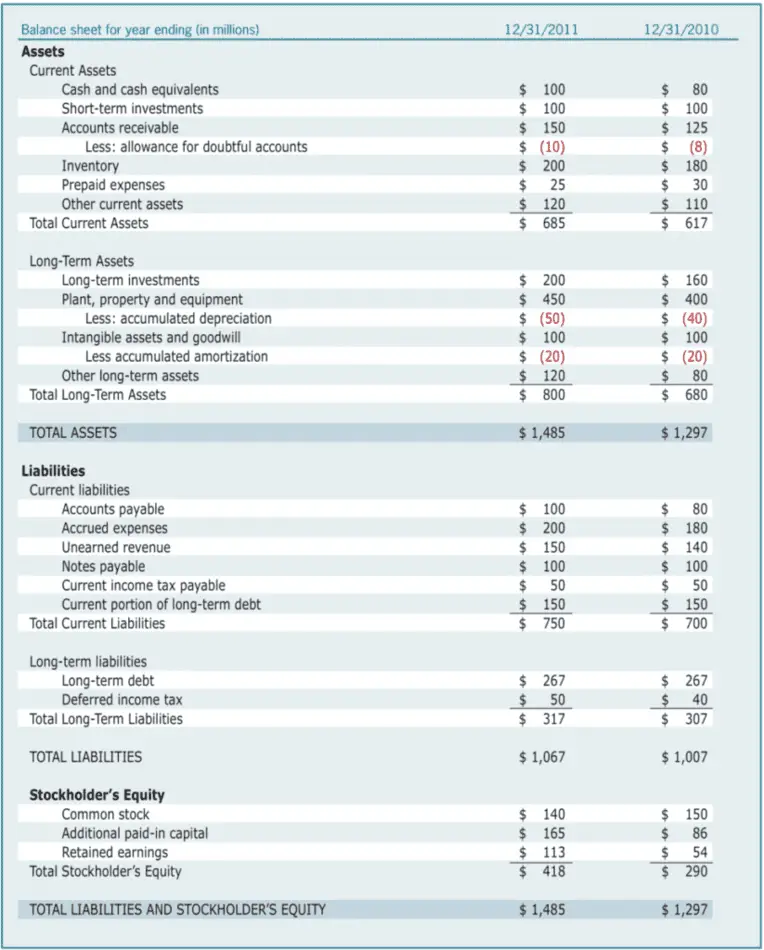

The balance sheet is the bedrock of a company. It shows the financial strength by listing all of the assets and liabilities at a single point in time, usually at the end of a fiscal quarter or year. It is found on the quarterly (10-Q), and annual (10-K) statements that are filed with the SEC and available on EDGAR. For foreign listed stocks, the information is normally found with the country’s government regulatory agency. The income, expenses, and cash flow that enter and leave a business are not shown; it is the overall effect of the transactions at a specific date.

There are three main segments to a company’s balance sheet: assets, liabilities, and shareholder’s equity. The statement gets its name because it must balance; assets equals liabilities plus shareholder’s equity. Assets are any company-owned or controlled resources to produce economic value. They represent ownership of value that can be traded for cash. Liabilities represent what is owed to another entity. They are obligations that require future payment in return for a benefit today. Shareholder’s equity is what would be returned to shareholders if the company sold all its assets and settled its liabilities. For example, if you had assets such as equity in a home worth $150,000, a car worth $20,000, and retirement savings worth $30,000, along with liabilities such as a mortgage of $50,000, credit card debt of $10,000, and some utility bills totaling $1,000, your shareholder’s equity would be $139,000 ($200,000 worth of assets minus $61,000 of liabilities).

Assets and liabilities naturally occur during business operations; a company may issue bonds (liability) in order to build a factory (asset). Both the factory and the bonds are recorded in the corresponding place on the balance sheet. Most companies report an itemized list of:

- Current assets (assets that can be sold within a year) – such as cash, short-term investments, accounts receivable, inventory, prepaid expenses, and other current assets

- Long-term assets (assets that cannot be easily converted into cash and are not expected to be sold within a year) – such as long-term investment; property, plant, and equipment; intangible assets; and other long-term assets

- Current liabilities (liabilities to be settled within a year, long-term liabilities (liabilities to be paid longer than a year)- such as accounts payable, accrued expenses, unearned revenue, notes payable, and income tax payable

- Shareholder’s equity- such as common stock, additional paid-in capital, and retained earnings

Assets

Current Assets

Current assets are classed as very liquid or readily convertible to cash and are expected to be used over the next year. On the balance sheet, they are listed in order of liquidity, with cash (such as money market funds and short-term Treasury bills) being the most liquid and prepaid expenses (such as rent, utility bills, and salaries) being the least. Asset-heavy industries, such as utility companies, are expected to have more cash on the balance sheet in order to pay for high Capex costs. In contrast, asset-light sectors, such as technology, do not need as much money. Cash levels can also be compared to other companies in the same industry to gauge strength in their particular environment. Too little cash may signal trouble, and too much may indicate that management does not know how to deploy capital effectively. Investors can use the current ratio (current assets minus current liabilities) to find the true level of money a company has on hand.

Accounts receivable is the amount other businesses owe in the form of credit to the company. If the figure is high, it may mean the company has relaxed credit terms or is having trouble collecting payments. Furthermore, if they are increasing rapidly, it may be a sign that they are relaxing their standards to boost sales. However, if accounts receivable is low, it may mean the company has short terms for its credit or is very efficient at collecting payments. Levels of accounts receivable can differ by sector; companies that produce high ticket items such as machinery will often have high accounts receivable, whereas cash-based sectors, such as restaurants, will generally have low accounts receivables.

Inventory refers to the goods and materials that a business holds for utilization, production, or resale. For example, steel is needed to make cars or cleaning supplies to clean an office. Inventory is required for companies to be able to operate and meet the demand of customers. If inventories are low, a business may be unable to produce a product or service, leading to lost sales. If inventories are too high, a company risks being unable to convert the inventory into sales and will therefore have value locked up and not being utilized. Balancing this level is particularly important in fast-moving industries, such as technology hardware, as the technology can quickly become out-of-date and unsellable. Too low, and the company will not fully maximize the opportunity.

Prepaid expenses are goods and services paid in advance, such as rent. On the balance sheet, they are first recorded as an asset, and then, as they are realized over time, the figure is recorded as an expense. For example, if a company pays for 12 months of rent for a building upfront, the whole 12 months’ rent is an asset. In the middle of the 12-month period, six months have been used and are therefore an expense, and six months have yet to be used and are therefore recorded as an asset.

Other current assets are often restricted cash (cash held for a specific purpose and not available for immediate use) and short-term loans.

Long-Term Assets

Long-term assets are not expected to be used or sold within the next 12 months. Long-term investments are stocks, bonds, or royalties the company intends to hold for longer than a year. Plant, property, and equipment are fixed assets that a company owns in order to operate. Their value is usually recorded as the original cost minus depreciation, which is written off as a non-cash expense over its estimated useful life. Each asset has its own rate of depreciation; for example, the life of a mobile phone is much shorter than the life of a factory. The management can also influence the rate of depreciation. Businesses may aggressively depreciate assets, raising expenses lowering profits, and therefore reducing the amount of tax owed. They may also take a slower depreciation rate to appear more profitable than they really are.

Again, long-term assets vary depending on the industry. Capex-heavy industries such as manufacturing will have many fixed assets, whereas a software company would be asset-light. Intangible assets are assets that are not physical, such as intellectual property and patents, which often have an expiration date and will lose value as they approach their expiration. Goodwill is the amount paid over the value of an asset. For example, if you were to buy Apple, you would pay vastly more than all its fixed assets because its brand adds enormous value to the company. However, because it is difficult to put a precise number on a brand’s value, goodwill can often be over or understated.

Total Assets

Total assets are just the sum of current and long-term assets. The figure is used in calculations such as a company’s book value (assets minus liabilities) and returns on assets (net income divided by total assets)

Liabilities

Liabilities represent what is owed to another entity. They are obligations that require future payment in return for a benefit today.

Current Liabilities

Current Liabilities are obligations that are due within 12 months. The most common current liability accounts payable; is the credit extended to the company by other companies, such as suppliers. The credit is reduced as goods and services are sold, and the proceeds are applied to the obligation. Accounts payable and shares should roughly rise and decline together. If accounts payable are increasing faster than goods and services sold, it could be a sign that the company is struggling to pay its bills.

Accrued expenses are expenses that have accumulated but have not yet been paid. The most common accrued expenses are rent and salaries. Unearned revenue is the revenue collected from an order for a good or service that is yet to be fulfilled. It is a liability because the business is required to fulfill the order within a pre-determined time. Notes payable is the short-term financing borrowed from lenders. Income tax payable is what is owed to the government, and the current portion of long-term debt is the long-term debt to be paid back that year. Companies must have enough current assets to cover current liabilities, or they will default or have to borrow more.

Long-Term Liabilities

Long-term liabilities are not expected to be paid within the next 12 months. Long-term liabilities include deferred income tax, pension obligations, and long-term debts such as bonds. The most common long-term liability is from the company issuing its own bonds that have scheduled interest payments. How the debt is used is vital to the health of the company. If it is efficiently allocated to sustainable profit-generating investments, it is an excellent use of a liability and does not dilute shareholders’ equity. If it is carelessly used, the company may not be able to generate enough cash flow to pay for the interest payments. Deferred income tax is the difference between the two methods of depreciation mentioned in “Long-term assets” and is recorded under long-term liabilities.

Total Liabilities

Total liabilities are just the combination of short and long-term liabilities. If the figure is equal to or more than total assets, it would mean the shareholders have no equity.

Stockholder’s Equity

Stockholder’s equity is what is left over after subtracting total liabilities from total assets. It can also be viewed as the company’s net worth, just as your total assets minus total liabilities equals your net worth. Common stock represents the shareholder’s equity, additional paid-in capital is the difference between the issuance of new stock (normally at market value) and what the shareholders paid for their shares. Retained earnings are earnings generated by the company, not returned to the shareholders through dividends. They are typically reinvested back into the business. Preferred stock is a hybrid between a stock and a bond. The share owner owns the company and receives a dividend but has limited voting power. However, in the event of liquidation, preferred stock has priority over common shareholders but after bond holders.